Minting on demand

Each AVA is powered by its own AVM, which mints AVAs in exchange for a corresponding reserve asset. For example, navETH is minted with ETH. An AVA’s supply begins at zero and grows only through purchases from the AVM. The exchanged reserve asset is deposited directly into the AVM’s reserves, where it becomes immutable, protocol-owned exit liquidity for AVA sellers. When AVAs are sold back to the AVM (redeemed), they’re burned, and sellers receive the reserve asset. This mint-on-demand model ensures that every AVA in existence was purchased fairly and that all tokens are backed by immutable, protocol-owned liquidity. There are no insider allocations.Price curve

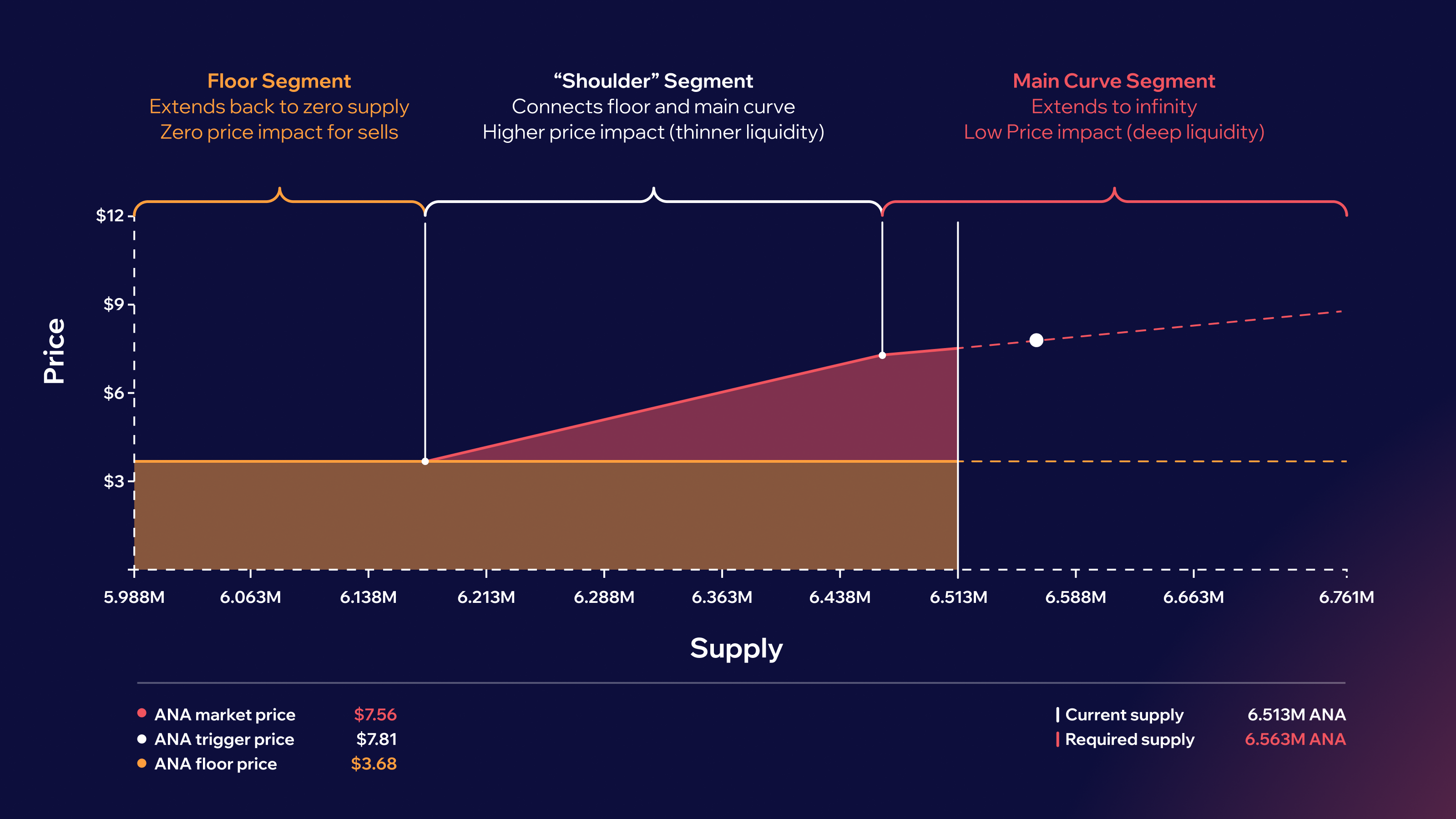

The AVM sets each AVA’s market price through a deterministic price curve:- Buys push the price upward.

- Sells push the price downward, but never below the floor.

- is market price

- is the floor price

- is current supply

- and are the supply thresholds where each section meets

- If supply is between 0 and the first supply threshold (s1), market price = floor price.

- If the supply is in between the thresholds (s1 and s2), market price is calculated from the shoulder slope equation

- If the supply is greater than the second threshold (s2), market price is calculated using the main curve slope equation